Summary of Thesis

- DCF Analysis shows a PT of $33.63, giving a potential 28% upside. Urban Outfitter’s comparables also show that the stock is oversold.

- The stock has been declining ever since hitting its high soon after Donald Trump was elected, and has declined ~36% since.

- The company’s stock has become underpriced after a sell-off due to the company not hitting its earnings estimates in Q3.

Overview of business

CEO and Chairman of the Board Richard Hayne co-founded Urban Outfitters with Scott Belair in 1970. They started with one store in Philadelphia, but they have since grown into a leading apparel company. Since becoming incorporated, they have expanded into five brands: Urban Outfitters, Anthropologie, Free People, Terrain, and BHLDN. In addition, they have expanded into the restaurant business after acquiring 6 Vetri Family restaurants, to give them a total of 12 Food and Beverage restaurants as of the beginning of 2017.

Each of their retail segments is geared towards a different audience. Urban Outfitters targets young adults, thus they suit the needs of this group by locating their stores in large metropolitan areas and select university communities and by creating an in-store environment likeable to this audience.

Anthropologie Group encompasses the Anthropologie, Terrain, and BHLDN brands. Urban Outfitters, Inc decided that the three brands complemented each other, thus the Terrain and BHLDN brands are incorporated into Anthropologie stores. Anthropologie caters to women aged 28 to 45 with its more sophisticated environment, while BHLDN focuses on elements of weddings. The Terrain brand is designed to offer home and garden products. The two Terrain garden centers that Urban Outfitters, Inc has also have their restaurants at the locations.

Lastly, the Free People brand has a retail side as well as a wholesale side that was created to achieve minimum production lots. The brand offers private label branded merchandise to young women aged 25 to 30.

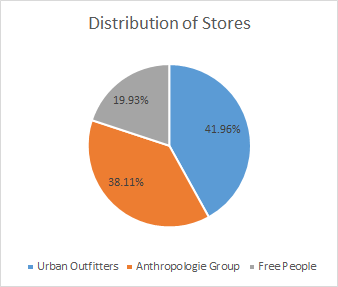

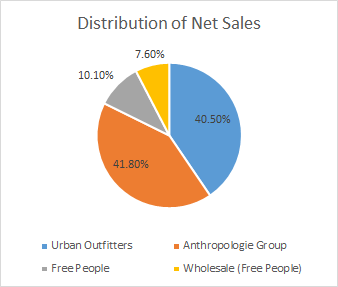

The following are distributions of how Urban Outfitters, Inc is spread across brands:

Source: Author's Calculations

Source: Author's Calculations

The pie charts show that the number of stores is fairly consistent with Net Sales, with Free People stores lacking in retail, but having a large number of net sales due to wholesale. Otherwise, Anthropologie stores are doing a bit better in net sales than Urban Outfitters ones.

Risks

Urban Outfitters, Inc has a few risks that should be discussed prior to an analysis of its growth and financials. A risk of importing issues has become an actual possibility under the newly elected President Donald Trump. If Congress does anything or something else happens to affect the flow of imports for Urban Outfitters, the company may experience a large increase in costs due to import taxes or not being able to ship their materials to the United States. [Edit: The import tax that Trump was planning to increase during his campaign was now called “too complicated” by him (Source: Marketwatch)]

Another risk that has turned into a reality over the holiday season is low traffic at Urban Outfitters retail locations. Urban Outfitters’s sales this holiday season were under expectations, and the stock price had reacted to the news, slipping around 11% pre-market, but quickly bouncing back up to normal levels. Low traffic is at risk of continuing due to a continuing decline in retail, but we will hope to see economic growth in the U.S. economy as a whole under President-elect Trump, which will increase expected sales for Urban Outfitters.

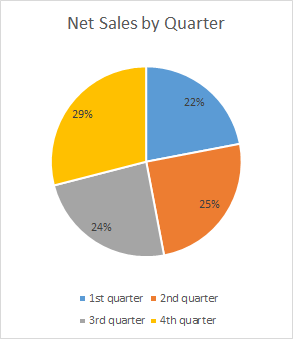

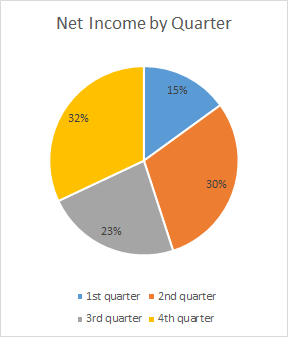

Furthermore, lower traffic during the holiday season will cause a lot larger problems than in any other quarter as the Q4 net sales and net income is the largest of any other quarter:

Source: Author's Calculations

Source: Author's Calculations

Future growth

On November 8th, $URBN was priced at 32.96, but in a matter of days it rose to a 52-week high of 40.80 after Donald Trump became president. Since that high, the stock has declined ~36%, closing at a price of $26.19 on Monday the 19th. The decline has been largely due to not meeting consensus estimates in the last quarter, Q3. Although this decrease in stock price was justified, I think $URBN has now become oversold since the last report. Thus, the newly depressed price has created a decent upside potential.

Although the company’s EPS did not meet the Street’s estimates, the company still showed good fundamentals in their Q3 presentation.

After creating a discounted cash flow model for the company, I came up with a target price of $33.63, representing a 28% upside. A few key assumptions were the following: a low single digit revenue growth (3% for fiscal 2017 and 3.7% thereafter) was conservative; however, an SG&A of 24.5% is probably moderate or aggressive even though it is similar to the past years’ SG&A. I ended up with a growing net income, and an EBITDA multiple of 5.5x, which ended up equating to a price target of $33.63. Something to note in addition to the DCF conducted using the EBITDA method was that the price target using the perpetuity method was by far larger than the former. This shows a great opportunity for growth as well.

Other than the DCF, even technical indicators, such as the RSI, which is 24.74 (Source: Finviz), show that this is oversold.

In addition to the DCF conducted, we can see how well Urban Outfitters, Inc is doing with its inventory and share repurchase program. While opening more and more stores, to increase net sales, the company has been able to increase its inventory while decreasing its costs. In addition, the company’s share repurchase program has largely decreased the number of shares outstanding and means that the company believes it has potential for future growth.

Comparison

When comparing the $URBN to the apparel industry as a whole and its related companies/competitors, Urban Outfitters, Inc also shows reasons for future growth. With a trailing PE ratio of 14.06, the company has a large upside when comparing this value to the trailing PE of the retail industry which is 23.62. Again, the lower the PE, the better, generally speaking, since it shows the price per share of the company’s stock is undervalued when comparing it to its earnings. The EBITDA multiple of $URBN is 5.5x, and when comparing this value to the apparel industry’s EV/EBITDA of 8.06x, once again, this shows that $URBN is undervalued.

Urban Outfitters, Inc top competitors are considered to be Abercrombie & Fitch (ANF), American Eagle (AEO), and Aeropostale (AROPQ). Out of these, URBN and AEO (American Eagle) have much higher profit margins than their competitors and fairly similar P/E ratios, thus, it may be that AEO is undervalued as well, but it has already started its climb even after reporting flat holiday sales. URBN has a net profit margin of 6.42%, while ANF has one of 0.38%, AEO’s is 6.62%, and AROPQ’s is -8.04%. URBN not only beats its competitors, but also beats the industry’s net profit margin which is 2.47%.

Lastly, URBN’s return on equity and return on assets are also very similar to AEO’s, but they still beat the industry average. One of the reasons AEO has done so well is that they were able to decrease their income tax from 44.3% to 33.7%, which was a huge decrease, allowing them increase their net income. Something else to mention regarding the two similar companies that are beating their competitors is that URBN only manages 596 stores worldwide (plus its 12 restaurants), while AEO has 949 stores plus its 97 stand-alone Areie stores. Thus, although the companies have similar metrics currently, I think URBN may have more potential for increasing revenue growth in the future.

Lastly, URBN’s return on equity and return on assets are also very similar to AEO’s, but they still beat the industry average. One of the reasons AEO has done so well is that they were able to decrease their income tax from 44.3% to 33.7%, which was a huge decrease, allowing them increase their net income. Something else to mention regarding the two similar companies that are beating their competitors is that URBN only manages 596 stores worldwide (plus its 12 restaurants), while AEO has 949 stores plus its 97 stand-alone Areie stores. Thus, although the companies have similar metrics currently, I think URBN may have more potential for increasing revenue growth in the future.

Conclusion

All in all, there are multiple methods of valuation that show that Urban Outfitters is currently undervalued and has a price target of $33.63 that should be hit by the end of the year, but AEO is also a company in the industry that is definitely worth analyzing further.

Lastly, if you have any comments please let me know in the comments section below. I have attached the full dcf model as well (in pdf format). If you have any feedback, I’d love to read that as well. Thank you for reading!